Everything homeowners in Scotland should know about Land and Buildings Transaction Tax (LBTT) in 2021

Whether you are looking for your next home, to purchase additional properties, or you are a first-time buyer, there are financial factors to consider beyond the property price. In this case, you may be charged Land and Buildings Transaction Tax (LBTT) when purchasing a new property.

If you are buying a home in Scotland before the 31st of March 2021, you may pay a reduced rate of Land and Buildings Transaction Tax (LBTT) due to COVID relief. However, as of the 1st of April 2021, Scotland will end the LBTT holiday of reduced rates and the standard rates of LBTT will return as normal.

What is Land and Buildings Transaction Tax (LBTT)?

The Land and Buildings Transaction Tax (LBTT) is a tax applied to residential and non-residential land and buildings transactions including any commercial leases and is administered by Revenue Scotland. Known as Stamp Duty in England, LBTT replaced UK Stamp Duty Land Tax in Scotland on the 1st of April 2015, following the passage of the Scotland Act 2012 and the subsequent Land and Buildings Transaction Tax (Scotland) Act 2013.

Simply put, the amount of Land and Buildings Transaction Tax you may pay, depends on the price of the property, or land, that you are buying. The amount of tax is payable at different rates on each portion of the purchase price within specified tax band.

How Much is Land and Buildings Transaction Tax?

There are different thresholds for LBTT to determine how much you may pay. Importantly, the tax you pay is calculated on the percentage of the property that falls above the threshold and it is a one-off payment that must be made no later than five working days of the ‘Payment Date,’ also known as the ‘Effective Date.’

For example, if you purchase a property for £180,000, you will be charged LBTT as follows*:

0% on the first £145,000 = £0

2% on the amount above the threshold, which is £35,000 = £700

Total LBTT amount to pay: £700

*Different criteria are set for first-time buyers and multiple property owners, please see following sections.

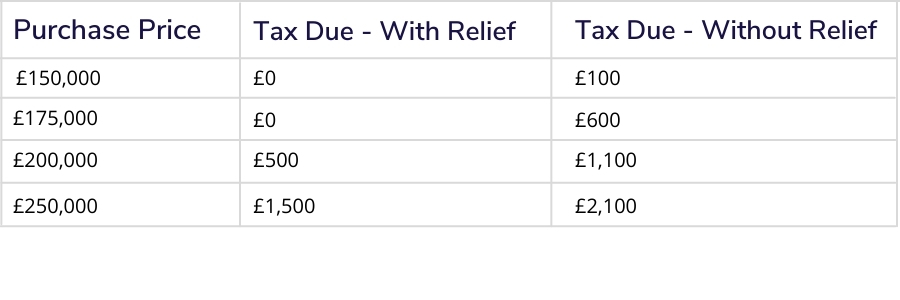

The Scottish Budget 2021-2022 confirmed that the ceiling of the nil rate band for residential LBTT will return, as planned, to £145,000 for transactions as of the 1st of April 2021. Therefore, the table below outlines the criteria as of April 1st, 2021:

How does LBTT apply to First Time Buyers?

If you are a first-time buyer, there is a relief available which increases the current residential purchase price from £145,000 to £175,000. This means that you will be charged 0% LBTT for any property up to £175,000. Additionally, if the property price is above £175,000, there is a reduction in tax of up to £600 available for first-time buyers, the criteria is as follows:

More information including first-time buyer FAQs is available on the Revenue Scotland website.

How does LBTT apply to people who want to buy a second home?

Buyers of additional residential properties, such as a second home, are charged 4% of the total purchase price of any dwelling over £40,000 or more. This is known as the Additional Dwelling Supplement, which was introduced on the 1st of April 2016 in attempt to protect opportunities for first-time buyers.

For example, if you purchase a second dwelling for £100,000, you will be charged LBTT as follows:

4% of £100,000 = £4000

Total LBTT due = £4000

For further information and examples of Additional Dwelling Supplement by Revenue Scotland, click here.

Am I charged LBTT on the total purchase price, or the asking price of a property?

LBTT is calculated by using the total purchase price. This means that if your offering price is higher than the asking price, you will be taxed on the higher amount if it falls above the threshold, as this is the actual purchase price. This is important to note when using online LBTT calculating tools, remember to put in the amount you are offering to achieve an accurate estimate.

When is LBTT not payable?

There are some circumstances whereby property buyers are exempt from paying LBTT. For example, if you inherit land or property under the terms of a will, you do not need to inform Revenue Scotland nor will you need to pay Land and Building’s Transaction Tax. The same applies if you receive property as gift, ensuring that there is no outstanding mortgage on it.

How can I find out the LBTT of a property?

To find out how much LBTT you could be liable to pay, there are several calculators available online:

Click here to use Money Advice Service’ LBTT calculator.

How can I pay LBTT?

In most cases, your solicitor will handle any Land and Buildings Transaction Tax due to be paid to Revenue Scotland by submitting the return on your behalf. However, as the property buyer, you are solely responsible to ensure it is submitted and on time (within 5 working days of the ‘Effective Date’). Please note you must still submit a return even if you fall below the threshold and are not due to pay LBTT.

To find out how to submit a return, click here.

So, if you are planning to join (or climb!) the property ladder, it is important to be aware of how LBTT could affect you financially. At Frazer Coogans, we will make sure you know this, and deal with the LBTT return on your behalf. If you have any further questions about LBTT, or are looking for a property solicitor, get in touch with us.